Five Tips for Reviewing Condominium Financial Statements

by Jason Roblin - September 30, 2019

by Jason Roblin - September 30, 2019

69

69

Over the last 10 years, there has been a boom in new condominiums in the Brandon market. Each new condominium corporation has a board of directors, with the majority being volunteer positions.

These volunteers come from a variety of backgrounds, some will have an excellent understanding of how to read financial statements and others may not have any experience at all.

Since the maintenance of a condominium complex is so important, managing the financial health of a corporation is one of the most important roles of the board members. Here are five tips on what to look for when reviewing the financial statements:

Focus on Comparative Figures — When the Statement of Operations (Income Statement) is presented, most are prepared with comparative figures. This allows board members to compare each line item for the current quarter to the budgeted performance, and last year’s results for the same quarter. It also allows a comparison for the year-to-date numbers. If the numbers vary, ask questions related to those specific items. For example, if snow removal increased by $5,000 for this year compared to the prior year and exceeds the budget by $2,000, what is the reason for the increase?

Is the corporation on track for a surplus or deficit? — In most cases condominium corporations are unable to borrow money from financial institutions, therefore if there is a deficit, it would have to be funded through increased collection of condominium fees or operating fees. If you are reviewing the second quarter financial statements and there is a budget shortfall (causing a potential deficit), you should inquire as to whether the deficit will be erased through normal operations by the end of the year. If not, an increase in condo fees might be warranted to prevent a special assessment in the future. If the corporation is on track for a surplus, chances are the operating fees are set at an appropriate level.

Reserve Fund – All condominium corporations in Manitoba are required to complete a reserve fund study. These reports look at replacing major items (driveways, roofs, etc.) that are the corporation’s responsibility. This includes an estimate of the replacement cost and a timeline for replacement. It is important to compare this information to the current balance in the reserve fund, and if necessary make recommendations for continued contributions to the fund so that the corporation is prepared when major items require replacement.

In the audited financial statements, there is often a note that states the percentage of the estimated future cost at the year-end date. It is important to know what that percentage is and what the strategy is to properly allocate money to the reserve fund. Corporations with reserve funds over 80 per cent funded are regarded as well-prepared for capital replacement. Be aware of where your reserve fund balance is at and what the strategy is to make sure the corporation is well-prepared for large expenses in the future.

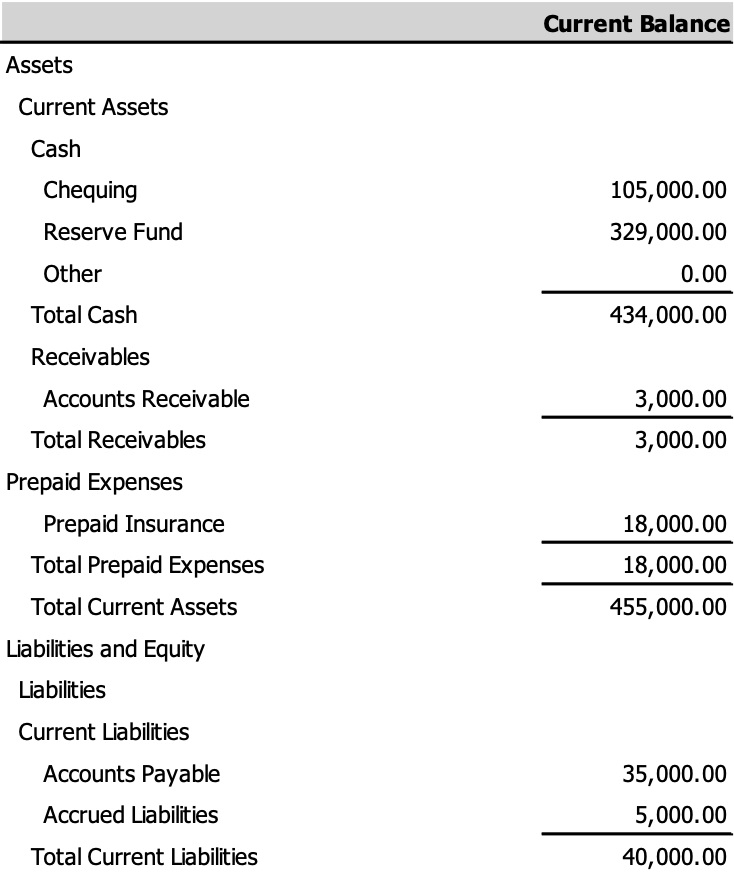

Working Capital – Review the liquidity of the corporation from the balance sheet (current assets minus current liabilities). Simply, take the operating bank balance then add accounts receivables and prepaid expenses, from there subtract accounts payable and accrued liabilities. That calculation will show the balance of the corporation’s working capital. If you take that number and divide it by the annual budget (divided by twelve), you will determine how many months of operating funds are currently available.

In this example, assume that the annual operating budget is $550,000. Working capital available today is 105K + 3K +18,000 – 35K – 5K = $86,000. Since the annual budget is $550,000, the monthly budget would be $45,800. This means there are 1.8 months of operating cash in the corporation. In this situation, it is likely that the corporation will be able to meet its financial obligations as they come due. If there is negative working capital, it is time to do a special assessment or raise fees so the corporation can meet financial obligations as they come due.

In this example, assume that the annual operating budget is $550,000. Working capital available today is 105K + 3K +18,000 – 35K – 5K = $86,000. Since the annual budget is $550,000, the monthly budget would be $45,800. This means there are 1.8 months of operating cash in the corporation. In this situation, it is likely that the corporation will be able to meet its financial obligations as they come due. If there is negative working capital, it is time to do a special assessment or raise fees so the corporation can meet financial obligations as they come due.

Additional Projects – Board members are often asked to approve expenditures that are either not budgeted for or exceed the amount in the budget. Here are some questions to ask to help deal with these situations.

- How much does the expenditure cost and how much will it put us over budget?

- Is there another budgeted item that we can cut to fund this expenditure?

- Is it something that can be deferred to next year, and properly budgeted for?

- If we are going to go over budget how are we going to pay for it (condo fee increase or special assessment)?

Vionell Holdings Partnership (VHP) provides rental housing and property management for an array of residential and commercial customers, including Condominium Management. VHP currently has over 4,000 units under management in Manitoba. For more information please visit www.vhproperties.ca.